Most people think that the point of entry for a reverse mortgage is age 62. For years, that was true. However, in 2018 a program was introduced that lowered the reverse mortgage minimum age to those that are aged 60 plus. Then a a few options became available earlier in 2021 that lower the reverse mortgage minimum age to 58. Now, as of September 2021, there is a new program that allows you to do a reverse mortgage at age 55 and up. The good news is, this program isn’t as conservative as the reverse mortgage for 60 year olds that came out in 2018.

First, What is a Reverse Mortgage in Plain English?

A reverse mortgage loan is a special type of loan that allows homeowners in California and Colorado to access a portion of their equity and convert it into usable funds.

If you happen to have a mortgage when you apply for a reverse mortgage, that loan will be paid off at closing thereby eliminating your mortgage payment. For most homeowners, the best part about a reverse mortgage is that there is no monthly mortgage payment for as long as they live or until they move out of their home permanently.

When you do this type of loan, you still own your home just like if you were to do a regular mortgage. Hence, you still have to maintain homeowner’s insurance and pay your property taxes and other applicable housing obligations like HOA’s etc.

Who Qualifies for the Reverse Mortgage at Age 55 Program?

That is a great question. From an age perspective, the point of entry is age 55 and up. Also, the property you’d like to get the reverse mortgage on should be your primary residence.

There are a ton of guidelines that accompany any mortgage program. We won’t bore you with 250+ page of guidelines. Instead, we’ll offer a short Q & A featuring some of the common questions, answers, features, and benefits of the new reverse mortgage program for homeowners under age 60.

Reverse Mortgage for 55 Year Olds Questions & Answers:

Question; Is this new reverse mortgage program affiliated with HUD, Fannie Mae, or Freddie Mac?

Answer; No, this reverse mortgage program for folks under age 62 is not affiliated with any of these entities. However, many lenders or brokers that offer the FHA insured reverse mortgage also offer this new program. Also, this loan is a non-recourse loan, just like the FHA version (similar to).

Question; Should I go to a Direct Lender or Broker for this program?

Answer; There are only a few investors that offer this program. In fact, there are only 4 investors that offer this program at the moment (03/09/2022). Any lender or broker that offers reverse mortgages can do them.

That said, there are a few distinct advantages of working with a mortgage broker.

First, brokers can align themselves with multiple lenders or investors. Hence, you’re not bound to the guidelines of just one lender like you would be if you worked directly with a lender.

Secondly, brokers shop for you. Due to that, brokers tend to offer more competitive pricing, rates, etc. A third item to consider is that often times brokers can get your loan done more quickly.

Question; Is it Hard to Qualify for the Reverse Mortgage at Age 55 Program?

Answer; As with any mortgage program, not everybody will qualify. Luckily, in some respects, this program is easier to qualify for that some other conventional mortgage programs.

Question; Are there Credit Score Requirements?

Answer; Yes and No. Don’t be discouraged by the numbers. We’d always encourage you to apply, especially if your FICO scores are close. That said, the basic credit score requirement is around 620. However, it can go lower, especially if you pass the financial assessment.

Question; What is the Financial Assessment & How does it Work?

Answer; With a reverse mortgage the most important part of your credit is your pay history on installment loans (like auto loans and leases) and housing expenses (mortgage, property taxes, HOA, etc). We look at your pay history for these items for the last 24 months. You’re only considered late if you’re 30 days late or more. You can generally have up to two late payments in the last 24 months.

Additionally, we look at your revolving account (i.e. credit cards) pay history for just the last 12 months. You can have almost an unlimited quantity of 30 day lates during the most recent 12 month period. However, it is a problem if you are 60 days late three or more times on these types of accounts in the last 12 months. Any payments made more that 90 days late will also be a problem.

Question; What is the Minimum and Maximum Loan Amount for this Program?

Answer; It depends on the investor, but the minimum loan amount ranges from $100,000 to $150,000. Some investors / lenders also have a minimum appraised value that ranges from $350,000 – $400,000.

For the maximum loan amount, that also varies. Most of them have a cap of $4,000,000 and some go to $6,000,000 (usually on an exception basis).

Question; Are There DTI Requirements?

Answer; the reverse mortgage program for homeowners under 60 does NOT have debt to income ratio requirements. We’ve made it easier to qualify. Basically, we total up all your monthly expenses that show up on your credit report AND your monthly housing expenses (taxes, insurance, HOA, and a funky calculation for what your utilities are likely to cost). In CA and CO, the residual income requirement is just $589 (for household of one) more than your other obligations. For a two person household, it’s $998 over your other obligations.

Question; What Kind of Income is Considered for the Reverse Mortgage at age 55 Plus Program?

Answer; This is another great question. Of course, all the normal types of income can be used like self employment income, w2 income, rental income, etc.

In addition to the NORMAL types of income, you can actually use assets as income with this reverse mortgage program. Assets includes things like che

cking, savings, stocks/bonds, cash value of life insurance, and even left over loan proceeds that were not used to pay off other loans at closing.

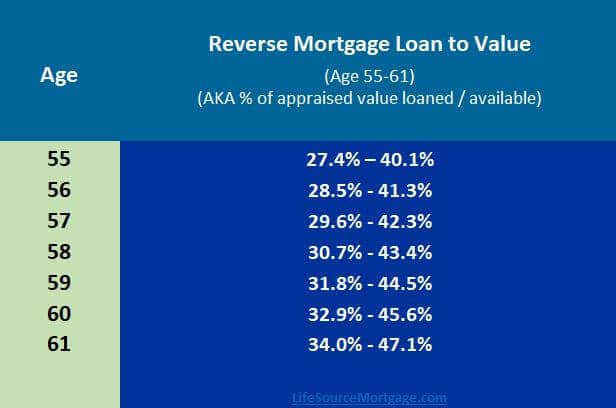

Question; What percentage of the appraised value can one borrow with this reverse mortgage program for 55 year olds?

Answer; It depends on your age. In fact, the amount you can borrow changes and increases with each passing year. To the right you’ll see a chart that shows the percentage of the appraised value you can borrow for each age bucket from age 55 to 61.

At age 62 plus a homeowner will then have the option to do this program or the FHA version. This program works best for higher end homes and higher loan balances. Again, with the reverse mortgage for 55 year olds, the amount or percentage you can borrow increases for each passing year up until age 88 where it caps out in the 52.1% – 62.3% range.

The FHA reverse mortgage has different LTV’s than this program. We’ll discuss those in a different article.

Want more info about the reverse mortgage at age 55 program? Email us at; [email protected].

Author; LifeSource Mortgage, California’s Best Mortgage Broker (Also licensed in Colorado and Idaho).