If you are looking for Jumbo Reverse Mortgage info, LifeSource Mortgage is a very well versed Jumbo Reverse Mortgage Broker in California, Colorado, and Idaho. In a classic question and answer fashion, we’ll teach you everything you need to know about these amazing proprietary or jumbo reverse mortgage programs.

What is the Minimum Age Requirement for Jumbo Reverse Mortgages?

When it comes to jumbo reverse mortgages (also know as proprietary reverse mortgages) the minimum age requirement may vary depending on the state you live in. However, as of 2022, the age requirement for jumbo reverse mortgage in Colorado, California, and Idaho is 55. Almost every investor has offerings with a minimum age of 55 in Colorado and California. When it comes to Idaho, there are less investors that allow you do to a reverse mortgage at age 55. As a top notch broker, we have strong relationships with all of the best jumbo reverse mortgage lenders. In other words, we’ve got you covered!

Reverse Mortgage Basics:

Just in case you’re not familiar with a reverse mortgage, here are the reverse mortgage basics. A reverse mortgage is a very safe, special, type of home mortgage loan that allows you to access a portion of your equity and convert it to usable funds. Otherwise, the equity in your home is meaningless (unless or until you sell your home). In the simplest of terms, a reverse mortgage is just like a regular mortgage except there are 3 key differences.

The first difference is that there is an age requirement. You have to be aged 62 or older for the FHA reverse mortgage. For the jumbo reverse mortgage in California, Colorado, and Idaho, you have to be aged 55 or older to qualify.

The second difference is that there is an equity requirement. While a regular FHA loan only requires 3.5% equity, a jumbo reverse mortgage has a bigger equity requirement (you can borrow anywhere from 38.1% to 60.4% of your homes value with a jumbo reverse loan). We’ll talk more in depth about the percentage you can borrow later.

The third difference as compared to a regular loan is that you don’t have to make a monthly mortgage payment when you do a jumbo reverse mortgage. However, you do need to maintain taxes and insurance since you still own the home when you utilize a jumbo reverse mortgage financing option.

Want more info about the jumbo reverse mortgage? Call us at (949) 492-2252 x704 or Email us at; [email protected].

Definition; What is a Jumbo Reverse Mortgage?

A jumbo reverse mortgage is a loan that can help California, Colorado, & Idaho residents access more equity than the FHA insured reverse mortgage. Now, there isn’t just one set loan limit for the FHA reverse mortgage. You see, every age bucket can borrow a different percentage of their home’s appraised value. For example, at age 62 you can borrow roughly 39% of your home’s appraisal value. So, if your home is worth $100,000 you can borrow $39,000 with the FHA reverse loan. At age 64 one can potentially borrow 40.1% or $40,100 if their home is valued at $100,000. The percentage you can borrow increases a little be with each passing year and caps out at about 72.99% for folks aged 92 and older.

What also comes into play with the FHA reverse mortgage is that there is something called a max claim amount. Simply put, the max claim amount is the maximum appraised value allowed by FHA. In 2022 the FHA max claim amount in California, Colorado, & Idaho (nationwide actually) is $970,800.

Now we know that a 62 year old can borrow 39% of the appraised value AND that the max appraisal value (for FHA) is $970,800.00. If you do the math, that means that the max FHA reverse mortgage loan amount is $378,612 ($970,800 x 39% = $378,612). On the other side of the spectrum the maximum loan amount for a 92 year old with the FHA program is $708,586 ($970,800 max appraisal X 72.99% = $708,586).

Colorado, Idaho, and California have many homes that are worth more than the FHA max claim amount of $970,800. For all intents and purposes, the definition of a jumbo reverse mortgage is one that allows homeowners to access more money than what the FHA reverse mortgage has to offer.

Want more info about the reverse mortgage? Call us at (949) 492-2252 x704 or Email us at; [email protected].

What is the Maximum Loan Amount for Jumbo Reverse Mortgages in California, Colorado, & Idaho?

At this point in time pretty much every investor or lender that offers jumbo reverse mortgages has a maximum loan amount of $4,000,000. However, most them will also make exceptions and potentially go as high as $6,000,000. While it is fairly common for the investors to make these exceptions, it’s also worth noting that they review each one on a case by case basis.

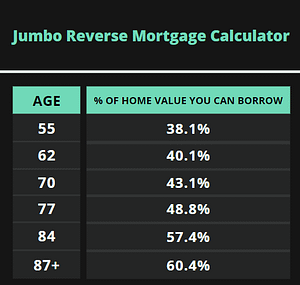

While these proprietary reverse mortgages are generally used for higher end homes with loan amounts that exceed those of the FHA reverse mortgage, that’s not always the case. For example, lets say that a 55 year old has a home that is worth $800,000. Let’s say they also owe about $200,000. As you know from the jumbo reverse mortgage calculator below, this 55 year old can borrow 38.1% of the value of their home. In dollars and cents, this 55 year old with an $800,000 home can borrow anywhere from $304,800. This certainly is not a jumbo sized loan, but the FHA reverse mortgage isn’t available to this 55 year old homeowner.

As you can see this loan can be used for other circumstances. So, this loan isn’t always jumbo sized and there is actually a minimum loan amount and it ranges from $100,000 to $150,000 depending on the lender or investor.

Jumbo Reverse Mortgage Calculator

Since there are so few jumbo reverse mortgage lenders (there are roughly 6 of them), there really are not any good, reliable, jumbo reverse mortgage calculators. Also, all of the lenders (and we work with all the best ones) percentage you can borrow is roughly the same AND if one makes a change, the others usually make the same adjustment.

mortgage calculators. Also, all of the lenders (and we work with all the best ones) percentage you can borrow is roughly the same AND if one makes a change, the others usually make the same adjustment.

With that said, we have taken the liberty of providing you with a chart that shows you what percentage of the appraised value you can borrow with each (right side of page) respective age bucket. Keep in mind that along with your age and your homes appraised value, the interest rate also dictates what percentage you can borrow with a jumbo reverse mortgage.

The percentage you can borrow also changes with every passing year (it goes up, so the older you are, the more you can borrow). In this jumbo reverse mortgage calculator / chart we’ll simply break it down for every 7 years or so. It starts at age 55 and then we end it at age 88 since that is the age where you can borrow the highest percentage of your home’s value.

Want more info about the reverse mortgage? Call us at (949) 492-2252 x704 or Email us at; [email protected].

What Type of Homes are Eligible for a Jumbo Reverse Mortgage In Colorado, California, & Idaho?

Most types of homes are eligible for a jumbo reverse mortgage. However, first and foremost, you can only use this type of loan on your primary residence. Beyond that, we’ll list both the eligible and ineligible property types for jumbo reverse mortgages below.

Eligible Property Types for Jumbo Reverse Mortgages:

- Single Family Residential (SFR)

- 2-4 unit properties

- Condominiums

- Townhomes

- Modular homes

- Mixed use properties (SFR, primarily residential, <25% used for business. Other restrictions may

apply).

Ineligible Property Types for Jumbo Reverse Mortgage:

- Manufactured Homes

- Cooperatives

Want more info about the reverse mortgage? Call us at (949) 492-2252 x704 or Email us at; [email protected].

What are the Payout Options for Jumbo Reverse Mortgages?

Presently, there are three different pay out options for jumbo reverse mortgage loans. We’ll discuss that here along with the potential advantages and / or disadvantages of each option.

Jumbo Payout Option #1

The most longstanding jumbo reverse payout option is a lump sum payout. In fact, for many years (from approximately 2007 to 2019 or 2019) the lump sum pay out was the only option with this program. It’s a simple concept, you basically receive your full benefit amount in one lump sum payout at closing.

The possible advantages are that you know exactly what you’ll get. If the market tanks, then you’re not subject to losing access to the funds like you might be with the other possible payout options. In addition to this, the lump sum payouts come with a fixed interest rate.

A possible disadvantage would be that since you’re using all the money up front it will accrue interest faster. You see, interest only accrues on what you use. Hence, if you don’t NEED to use all the money up front, you may want to consider one of the other options so that your loan balance doesn’t increase as fast thereby protecting your homes equity and estate.

Jumbo Reverse Payout Option #2

Want more info about the reverse mortgage? Call us at (949) 492-2252 x704 or Email us at; [email protected].

There is an exciting newer payout option that came out in around 2021. It’s an option that’s long been available with the FHA program and it’s the line of credit option. It’s pretty basic. You’re awarded a line of credit that would be the same as your lump sum payout amount (depending on how you structure the lump sum payout option). Then, you use the funds when you need them. They have a couple of rules though. For example, you have to use at least 25% of your available loan amount at closing. On the opposite side of the spectrum, you can only access up to 90% of the total amount available at closing.

With the line of credit option, you have access to the line of credit for up to 10 years.

Here are a couple of possible advantages of selecting the line of credit pay out option. The biggest advantage is that since interest only accrues on what you use, it reduces that speed at which your loan balance grows. In turn, this means it protects your equity as well as the equity of those that stand to inherit your home. Another minor advantage is that your unused credit actually grows at 1.5% per year for the first 7 years.

And now for the possible disadvantages of doing the jumbo reverse mortgage with a line of credit payout option. First, the line of credit could potentially be cut off if there was a significant downturn in the market (like what happened in 2007 -2008). Also, The start rate is about 5.5% right now. There is a cap that is 5% over your start rate. Hence, your line of credit interest rate can potentially go as high as 10.5%.

Jumbo Reverse Mortgage Payout Option #3

This payout option sort of goes in conjunction with the line of credit option. Based on your available loan proceeds, you can get monthly payments sent to you for anywhere from 24 to 120 months. We refer to this as a term payout option.

The advantage might be that you preserve your equity and you have a guaranteed payment coming in for anywhere from 2-10 years.

One of the disadvantages is that the payments can only go for 10 years maximum.

Want more info about the reverse mortgage? Call us at (949) 492-2252 x704 or Email us at; [email protected].

Proprietary Reverse Mortgage (aka Jumbo Reverse) Safeguards

In some respects, the jumbo reverse mortgage has similarities to the FHA version of this loan. Below are a couple of the safeguards put in place that are resemble the FHA reverse loan.

- Prospective borrowers have to complete a counseling session to ensure they are aware of their options and their required obligations pertaining to the loan.

- Like the FHA loan, the borrower has to pass a financial assessment. The financial assessment is pretty basic, but we just like to make sure that you have the means to maintain property taxes and insurance. It’s not too daunting, so don’t stress.

- Similar to the FHA reverse loan, the proprietary / Jumbo reverse mortgage is a non-recourse loan.

What does non recourse loan mean exactly? It means that no other assets can be used to repay the loan. Only the collateral can be used the repay the loan. So, if the market crashed after you took the reverse mortgage and you ended up owing more that what your home is worth, your OTHER assets are protected. You’d never be on the hook for a debt that exceeds the value of your home.

How Much are the Jumbo Reverse Mortgage Closing Costs?

This is a very good question. However, it does depend on how the loan is structured and the loan amount. When you do a reverse mortgage, there’s 3 potential buckets of fees.

Firstly, there can be a Mortgage Insurance Premium. However, this only applies to FHA reverse mortgages and NOT jumbo reverse mortgages. That’s one nice feature of the proprietary reverse program.

Secondly, there could be an origination fee that goes to the broker or the lender.

Thirdly, there are the normal 3rd party fees like any other mortgage loan (would include things like county recording fees, appraisal, title insurance, etc.).

With all of that said, often times there are no cost options because the lender or broker may be able to offer a lender or broker credit to pay for the closing costs. The only exception is that FHA (even though the jumbo is not an FHA loan) does not allow for lenders or brokers to pay for the counseling fee and recording fees).

Want more info about the reverse mortgage? Call us at (949) 492-2252 x704 or Email us at; [email protected].

Proprietary & Jumbo Reverse Mortgage Interest Rates

The interest rates associated with jumbo reverse mortgage loans depends on how you structure it. With that said, they range from 5.9% to 9.15%. If you’re thinking that’s on the higher side, think again. From roughly 2008 to 2015 or so, there was only one jumbo reverse mortgage lender and it’s interest rate was either 8.75% or 8.875%. Then, around 2015 more lenders entered the space and due to that and a lower mortgage interest rate environment, the interest rate offerings got a little better and dropped to the 4.9% – 7.15% range. ***NOTE, in 2022 (and 2021) interest rates have shot up SO much and so quickly historically speaking, that these numbers may or may not be perfect. Please call for current info.

If I am Age 55 Plus, but my spouse is not, can we still do a reverse mortgage?

This is a very good question. It depends on the investor. Some lenders / investors will allow this and some will not. With that being said, it’s really important to understand that ONLY the borrower’s on the loan reserve the right to live in the home until their death without making a monthly payment.

Do I Need Income to Qualify for a Jumbo Reverse Mortgage?

The answer to this question is “yes” and “no”. This loan is alot easier to qualify for than a regular loan that has a monthly payment. With a regular loan, your monthly income needs to be at least double your monthly obligations (credit report debts, property taxes, insurance and mortgage payment). With a reverse mortgage we look at what’s called residual income and you simply need to make about $550 more than your credit report debts, property taxes, and homeowner insurance. This applies to a “one” person household. If you live in a “two” person household, you need to make about $950 more than those items. Hence, it’s alot easier to qualify.

We can use all the normal income items like a regular loan (i.e. social security income, pension, w-2 income, self employment, etc.), BUT was can also use liquid assets AND loan proceeds as income. Obviously, that is unique, and again it just makes it easier to qualify versus a regular loan.

LifeSource Mortgage, California, Colorado, & Idaho’s Best Mortgage broker offers both the FHA insured reverse mortgage and the proprietary jumbo reverse mortgage options.